Date : 26/08/2024

DCF Model created, article written by Rishabh Jain

Summary & Notes:

- HDFC Bank Limited is an Indian banking and financial services company headquartered in Mumbai. It is India’s largest private sector bank by assets and the world’s tenth-largest bank by market capitalization as of May 2024.

- HDFC Bank has Market cap of around 12.4 lakh crore, and total assets of around 40 lakh crores. And the Bank holds total deposits of around 23 lakh crores.

- Total Cash (Current Asset) as of March, 2024 is 2.28 Lakh Crores, while Total Deposits as of March, 2024 are 23.7 Lakh Crores. 10% of Total deposits is around 2.37 Lakh Crores, which means Bank holds Decent Cash to cover any short-term Cash requirements.

- Debt to Equity Ratio of the Bank is around 6.81, which is high compared to non-financial Industry, but for Banking Industry, D/E ratio of 6.81 is similar to other Banks in the country and close to average D/E of Banking Industry. As long as Loans are well managed with low Defaults, etc, this is manageable.

- Revenue and Profits of the company have grown almost 10x from 2013 to 2024, where Revenue grew from 35.8 Thousand Crores (2013) to 283.6 Thousand Crores (2024), while Net Profit grew from 6.9 Thousand Crores (2013) to 65.4 Thousand Crores (2024).

- Current Year’s Return on Equity is around 17.1%, while 5 year average return on equity is 16.8% (per annum).

- PE Ratio of the company is around 18.3, while Median PE ratio of Banking Industry is around 11.9. which means Market is favouring this Bank over others even if they have to pay more price for earnings.

- Weighted Average cost of capital (WACC) for HDFC Bank came out to be 9.3% according to my analysis. It can be considered slightly high, I expect it to decrease in future years, which can further increase DCF value.

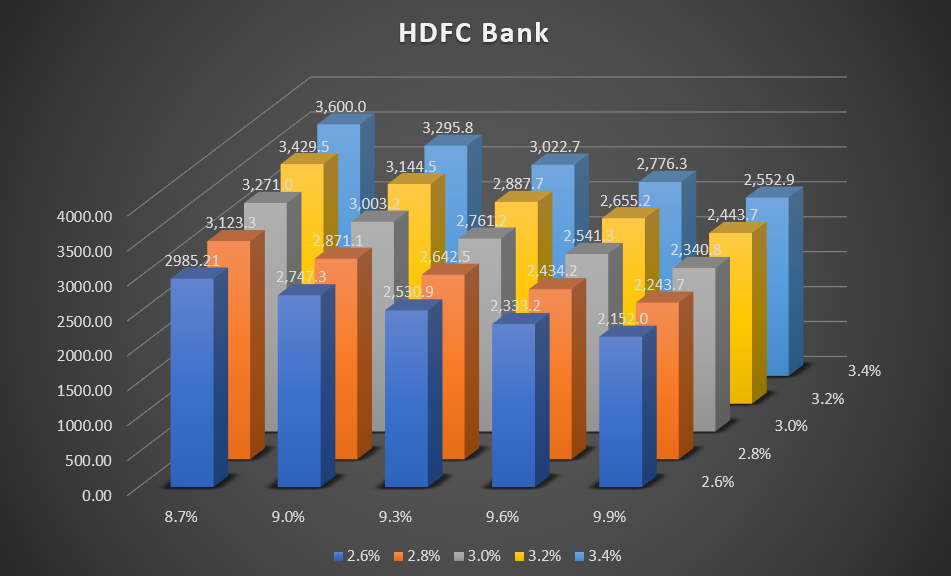

- Intrinsic Value for HDFC Bank came out to be around 2756 rupees per share, in Base case Scenario. This valuation relied heavily on Terminal value (84%) and less on DCF of next 5 Years (16%). According to my analysis, future growth after next five years will still be quite significant, this valuation model signifies that.

- HDFC Bank has strong and efficient Management, you don’t see Companies with such high Market Cap like HDFC Bank to grow their Revenue and Profits almost 10x in past decade. Can HDFC Bank Grow its Revenue and Profits 10x again in the next Decade? Let’s wait and see what next decade looks like for HDFC Bank and Banking Industry in general.

Discounted Cash-Flow Model:

Cases and Assumptions:

| Cases | 1 | 2 | 3 |

| Revenue Growth(%) | 25 | 20 | 15 |

| Operating Expenses % of Revenue | 54 | 56 | 58 |

| Employee Expenses % of Revenue | 8.5 | 8.9 | 9.3 |

| Current Liability Growth % | 16 | 15 | 14 |

| Terminal value Growth rate % | 3 | 3 | 3 |

DCF Model Excel File (Download Below)

Excel File Includes:

- Forecasts on Revenue, COGS, R&D Expenses, Depreciation& Amortisation

- Forecasts on Current Assets & Current Liabilities.

- Calculation of Working Capital, CAPEX, Free Cash-Flows.

- Calculation of Weighted Average Cost of Capital.

- Calculation of DCF Intrinsic Value per share of the company.

- Added Graphs for Visualisation of the data.

Disclaimer :

This DCF Model is for Educational and Research purposes ONLY. The DCF model was based on several Assumptions, and it doesn’t Guarentee it will happen in future. This is not in any form a Financial Advice. Do your own Due-Diligence for Investing. For more details visit our Legal Page –https://r1hedge.com/legal/

Check my other Posts:

How to Value Stocks, Valuation

DCF Model on GOOGLE Alphabet Class C, GOOG

DCF Model on ADANI Enterprises, ADANI

Book Recommendations, Books.

Pingback: Fundamental Analysis of Canara Bank, DCF Model | R1Hedge - R1Hedge