DCF Assumptions and Scenarios

| Cases: | 1 (Optimistic) | 2 ( Base Case) | 3 ( Pessimistic |

Reveue Growth | 10% | 9% | 8% |

| COGS (% Revenue) | 43% | 44% | 45% |

| Current Assets Growth | 9% | 8% | 7% |

| Current Liabiliies (Growth) | 11.65% | 12% | 13% |

| Growth Rate (Terminal Value) | 1.2% | 1.2% | 1.2% |

DCF Model Excel file :

File Includes :

- Forecasts on Revenue, COGS, R&D Expenses, Depreciation& Amortisation.

- Forecasts on Current Assets & Current Liabilities.

- Calculation of Working Capital, CAPEX, Free Cash-Flows.

- Calculation of Weighted Average Cost of Capital.

- Calculation of DCF Intrinsic Value per share of the company.

- Added Graphs for Visualisation of the data.

Summary and Notes:

- Google is a Stable Company with Good long-term Prospects and relatively low Debt Levels. Debt/Equity Ratio is 13.13%. Effective Interest rate on Long term debt is around 1.33% which is very low and manageable.

- I expect Revenue to grow higher than average industry in US.

- Even at Base case Scenario and considering Companies reputation, Google is Fairly Valued in the market. It would be Buy and Hold for the company under given assumptions and scenarios.

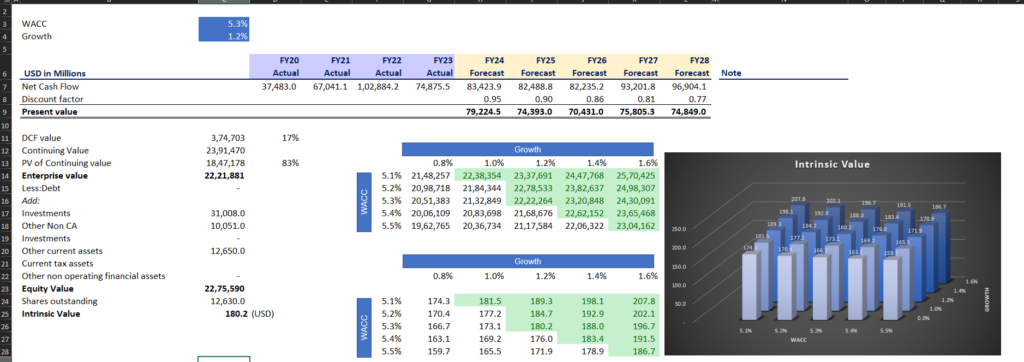

- WACC came out to be 5.3%, which is relatively high for the company, because of current US economy with high interest rates on US Government Bonds. I expect it to decrease in coming years when US economy grows, So that could also make Google undervalued at current price.

- Intrinsic Value per share came out to be $180 per share, which almost matches its current price in the market. Which makes it Fairly valued given our assumptions.

Disclaimer

This DCF Model is for Educational and Research purposes ONLY. The DCF model was based on several Assumptions, and it doesn’t Guarentee it will happen in future. This is not in any form a Financial Advice. Do your own Due-Diligence for Investing. For more details visit our Legal Page –https://r1hedge.com/legal/

Check out My Book Recommendations

Book Recommendations : https://r1hedge.com/book-recommendations/

Pingback: DCF Model, Intrinsic Value of Adani Enterprises | R1Hedge - R1Hedge

Pingback: DCF Model, Intrinsic Value of HINDALCO | R1Hedge - R1Hedge